Every monthly mortgage payment consists of a few different expenses. The type of loan you chose will determine if some of these expenses are a part of your mortgage or not. For instance, if you’re going with a conventional loan, you can put 10% or more down to remove the need for anything other than the principal and interest payment to the lender. Although on ALL government loans, you’re required to keep your taxes and insurance impounded and a part of your mortgage payment!

So what are impounds in a mortgage payment?

Impounds are escrows. And if you don’t know what either are that’s okay! Simply put, escrows are expenses that are held in an escrow account that are to be paid at a later date. In the same sense, you would impound certain fees into an account to disburse them at a later date. So escrows and impounds are the same exact thing; money set aside to pay the tax, insurance and other real property bills when they become due.

Since real property can suffer from tax liens and natural disasters, many lenders will require you impound these items to protect their position against the title of your home. When these costs are impounded, the lender will collect equal monthly installments for each and make sure there is never a lapse in coverage or a missed tax payment. But this isn’t required on all loans.

See the table below:

Conventional – 10% down or more: you can remove impounds

FHA – Must always include impounds

VA – Must always include impounds

USDA – Must always include impounds

Non-QM – Typically follow conventional rules

Jumbo – Rules vary per lender, but generally follow conventional rules

Now that you’re more familiar with impounds / escrows, here is what a mortgage payment typically consists of when these items are required:

- Principal and interest – Each mortgage payment will have a principal and interest payment. This payment is the payment to your lender and will eventually pay down your balance. You can make this your only payment with conventional financing and a down payment equal to or greater than 10%

- Homeowners insurance (HOI) – You will make equal installment payments to this category so that your lender can pay your homeowners insurance bill each year when it’s due.

- Property Taxes – Your tax bills for real property are typically due twice a year. Once in March and once in October. However you can avoid costly semi-annual bills by wrapping these up in your mortgage. You will pay equal installments to your lender each month and they will pay these installments when they become due.

- Mortgage insurance – Your mortgage insurance payment can and will be included in your mortgage payment if you’re on a monthly mortgage insurance plan. In the case of an FHA loan, mortgage insurance is almost always required.

- Additional tax assessments and insurance premiums – Any additional tax assessments and insurance premiums that need to be impounded in your mortgage payment can be included too; flood, wind, fire, tornado etc…

*Note, an HOA fee or fees are NEVER included in your mortgage payment*

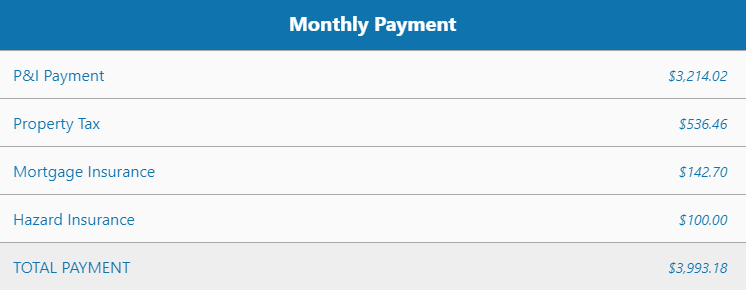

Example Payment:

*Payment put together on the cracked calculator found on www.grahamjay.com